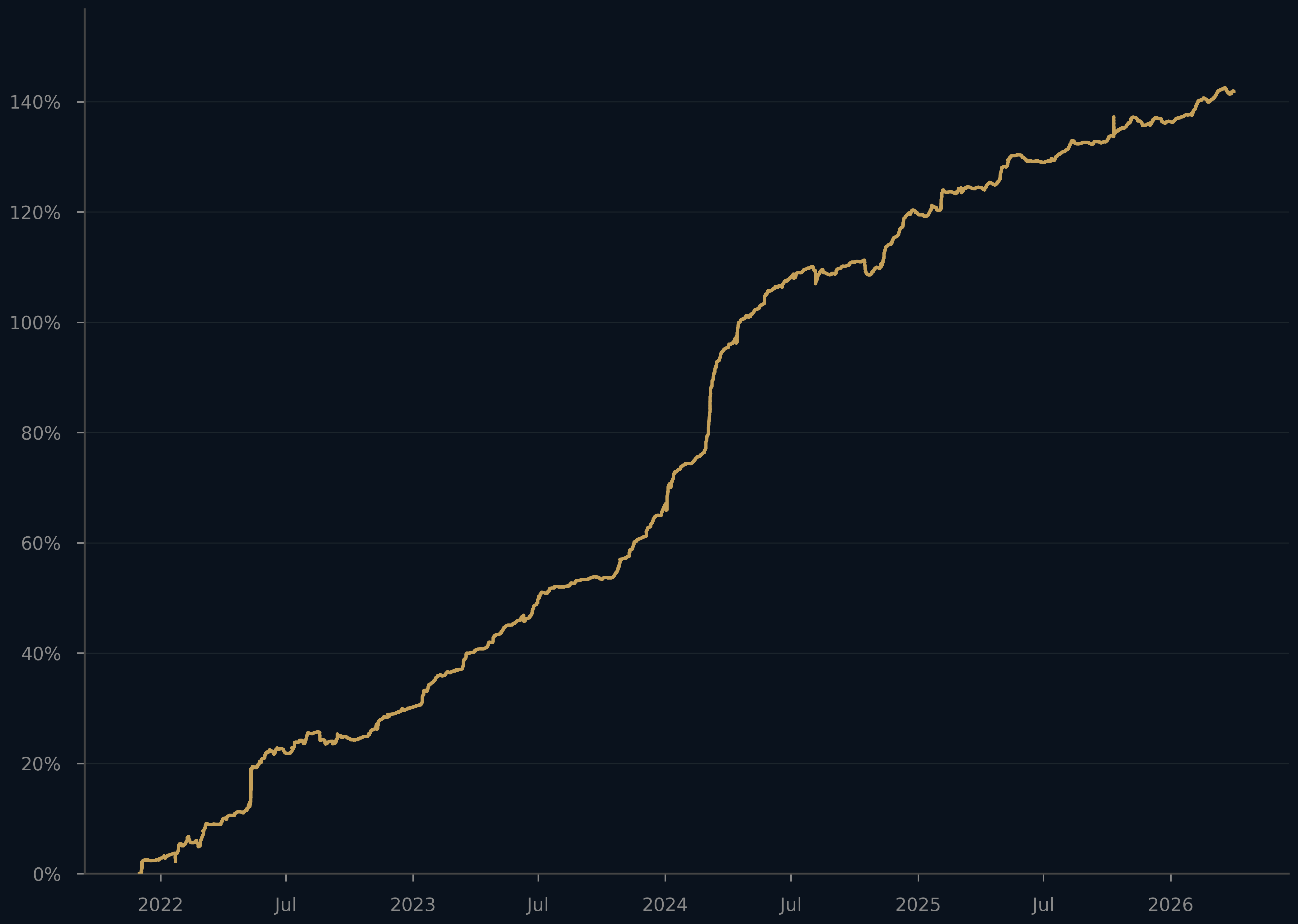

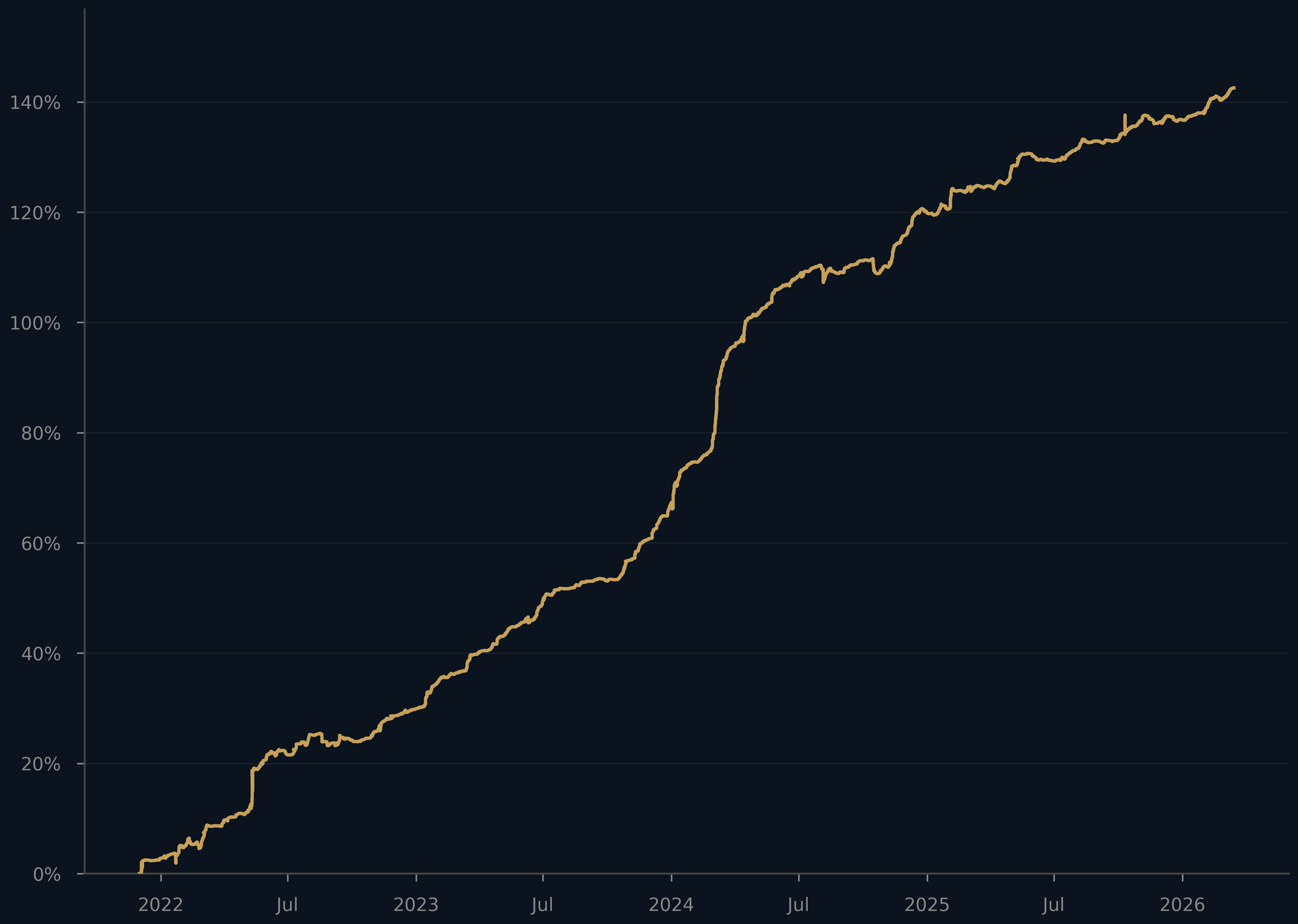

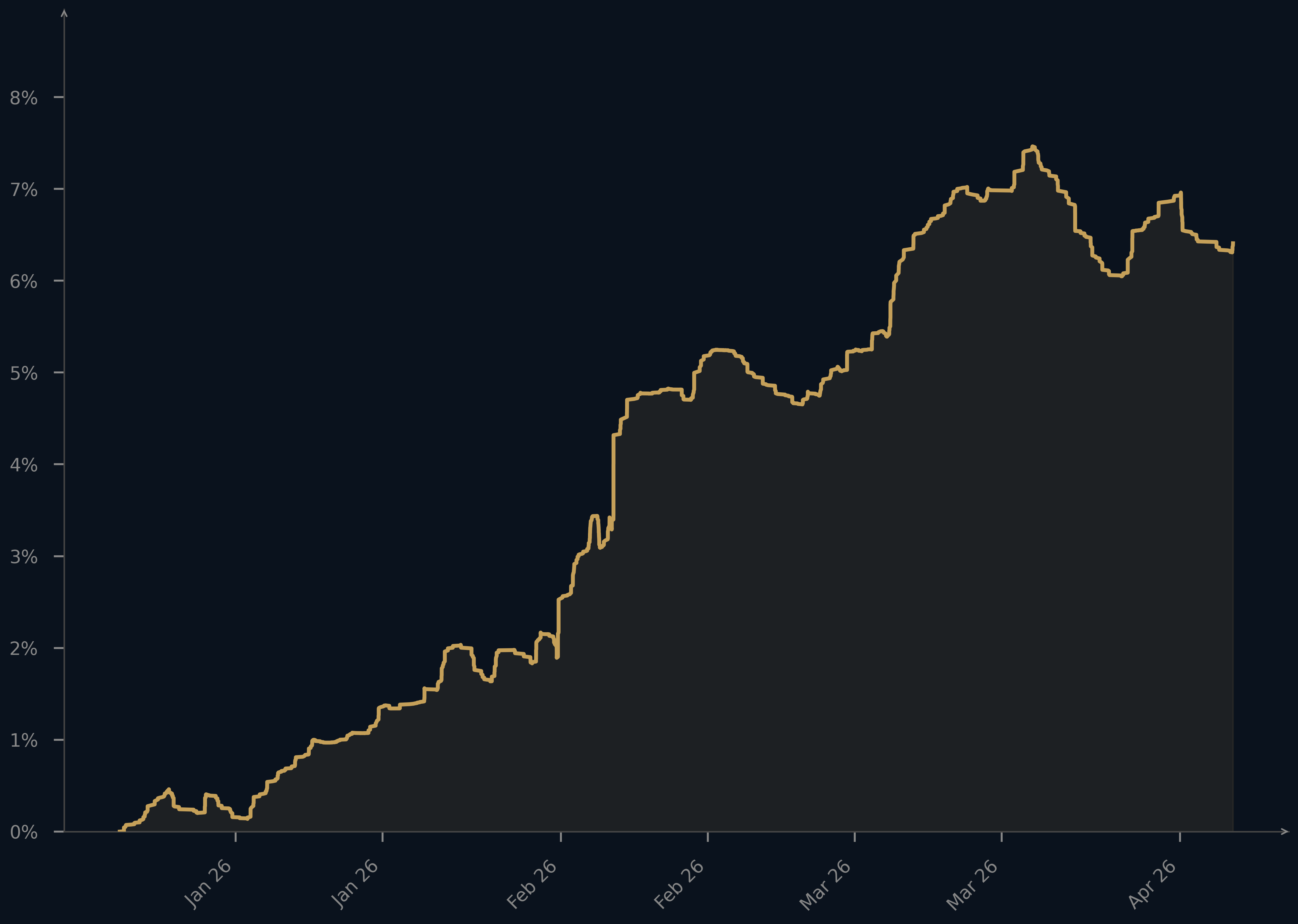

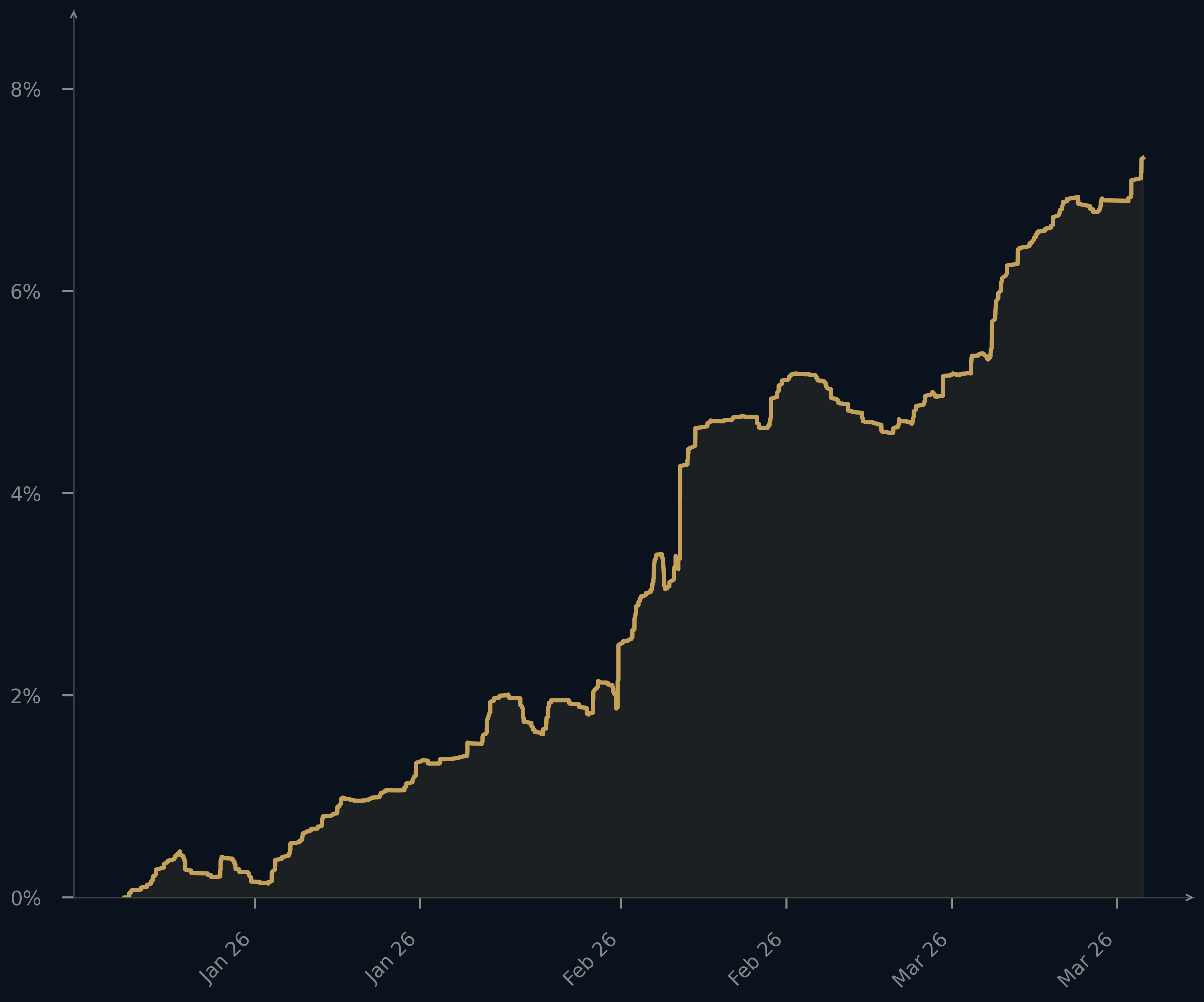

Strategy Portfolio

Complementary by Design

QuantVision operates a unified adaptive portfolio built on two complementary strategy pillars.

Trend-following

Exploits the momentum of the market by identifying and riding established directional price movements until they show clear signs of reversal.

Mean-reversion

Exploits the statistical tendency of an asset's price to revert to its fair value after deviation.

Instead of binary exits, we employ multiple risk constraints to limit downside. This ensures structural stability while keeping our strategies active across all market conditions.

Strategies are always deployed, while capital allocation and exposure are dynamically adjusted as market conditions evolve. The portfolio is engineered so that strategies compensate for each other across market conditions, with predefined limits ensuring that underperformance in one pillar cannot become structurally damaging to the whole.